Momentum in the buy now pay later (BNPL) space is remarkable in every way: Afterpay and Affirm are still growing GMV close to or at triple-digit figures, exits are proving to be massive, and fundraising is relentless - as of Sep’21 YTD, BNPL funding was already 2x higher than all of 2020.

BNPL has not only grown quickly, but has also evolved as a business model. What started out as a checkout feature at a select group of in-network merchants has transformed into a consumer-led product that can be used for any purchase. The implications of this shift in the BNPL model points to a larger trend beyond the scope of BNPL: the unbundling of traditional credit cards, which in turn opens up a myriad of opportunities for startups across the fintech ecosystem.

BNPL 1.0

The original BNPL model that was popularized was an interest-free, “pay over X” model - typically 4 equal payments over the course of 6-8 weeks from Klarna/Afterpay. Affirm introduced a longer duration model: a monthly installment plan, typically 12-48 months, with varied APR.

BNPL grew in popularity, as it proved to be a win-win for both merchants and consumers. Merchants appreciate the higher AOV on BNPL purchases, greater cart conversion and repeat purchasing. The resulting boost in revenue typically more than makes up for higher fees (merchants pay ~6% to the BNPL providers). On the other side, according to a recent BofA study, consumers appreciate that BNPL helps them manage budgets, allows them to pay in installments, and offers good in-app shopping deals.

This “BNPL 1.0” model did well, but was limited in scope through the distribution method: merchants first had to activate the BNPL offering on their online checkout flow, and then consumers had to choose it when making the purchase online. BNPL 2.0 removes this two-step process, and turns it into a more frictionless consumer-led experience.

BNPL 2.0: BNPAL (“Buy Now Pay Anything Later”)

As the large BNPL players (Affirm, Afterpay, Klarna) grew and gained millions of customers along the way, their offerings evolved. They have all introduced in-app shopping marketplaces and have “Super App” ambitions.

Recently, each has also introduced products allowing customers to “buy now pay anything later.” Why limit customers to in-network merchants, when instead you could offer a BNPL product for all consumer purchases?

Both Klarna and Afterpay are enabling this offering through their apps; Affirm is taking it a step further with a product they just announced called Affirm Debit+. As the website claims, “Buy now, then decide [later] if you want to split purchases into budget-friendly payments.” The debit card comes with an app, which allows consumers to choose which transaction to turn into an Affirm pay-over-time product.

Unbundling of the Credit Card

The natural question to these “buy now pay anything later” offerings is, “how are they any better or different than a credit card?” The answer lies in understanding the “job to be done” for the consumer, and which offering fulfills that better.

As Simon Taylor pointed out recently, managing cash flow is a critical job-to-be-done for consumers that credit cards purport to solve. However, credit card offerings and programs have hardly evolved over the past two decades. As he continues, a credit card “doesn’t allow you to manage your cash flow or finances as easily; it is hard to control, expensive and often leads to debt.”

Following the GFC, there has been a fundamental change in attitude, with younger consumers becoming wary of credit, and many switched to their debit cards. Credit cards haven’t kept up with consumers’ needs for what a healthy credit product should provide.

"[There was] a generational shift - young people coming of age after the financial crisis of 2008 were no longer willing to tolerate getting into permanent debt by putting it all onto the card or getting burned with late fees and interest. These young consumers and many like-minded older ones grew fundamentally suspicious of credit and retreated into the simplicity of their debit cards.”

— Max Levchin, CEO Affirm

On the other hand, BNPL gives consumers the flexibility and control they want to manage their cash flow, and offerings continue to improve. The Affirm Debit+ card gives a sneak peek into the future of BNPL. Today, it offers consumers the ability to choose which transactions to pay up-front for or split over time.

Going forward, they expect to offer both short and longer-duration installment options, giving consumers the flexibility and control they appreciate in BNPL in an everyday spending card. One can imagine a future where consumers are offered personalized rewards and discounts, coupled with complete control over financing options and durations, allowing them to seamlessly mix and match the financial options that work best. This adaptive consumer product is a far cry from the rigid credit card that young consumers have become wary of.

The disruptive force of BNPL points to a broader trend that is well underway: the unbundling of credit cards. Large financial institutions generate an incredible amount of revenue on credit cards, and a new generation of companies will also succeed by unbundling their offerings with better, consumer-friendly products that better serve the younger generation and the dynamic world we live in.

The opportunity is massive: $8T in consumer credit, $121B in credit card interest charges, $11B in overdraft fees, $3B in late fees; overall bank non-interest income was ~$250B in 2019.

These amounts are staggering, and while BNPL has small market share today, growth rates suggest market share will increasingly shift to BNPL over the next decade.

What is Lithic doing with BNPL?

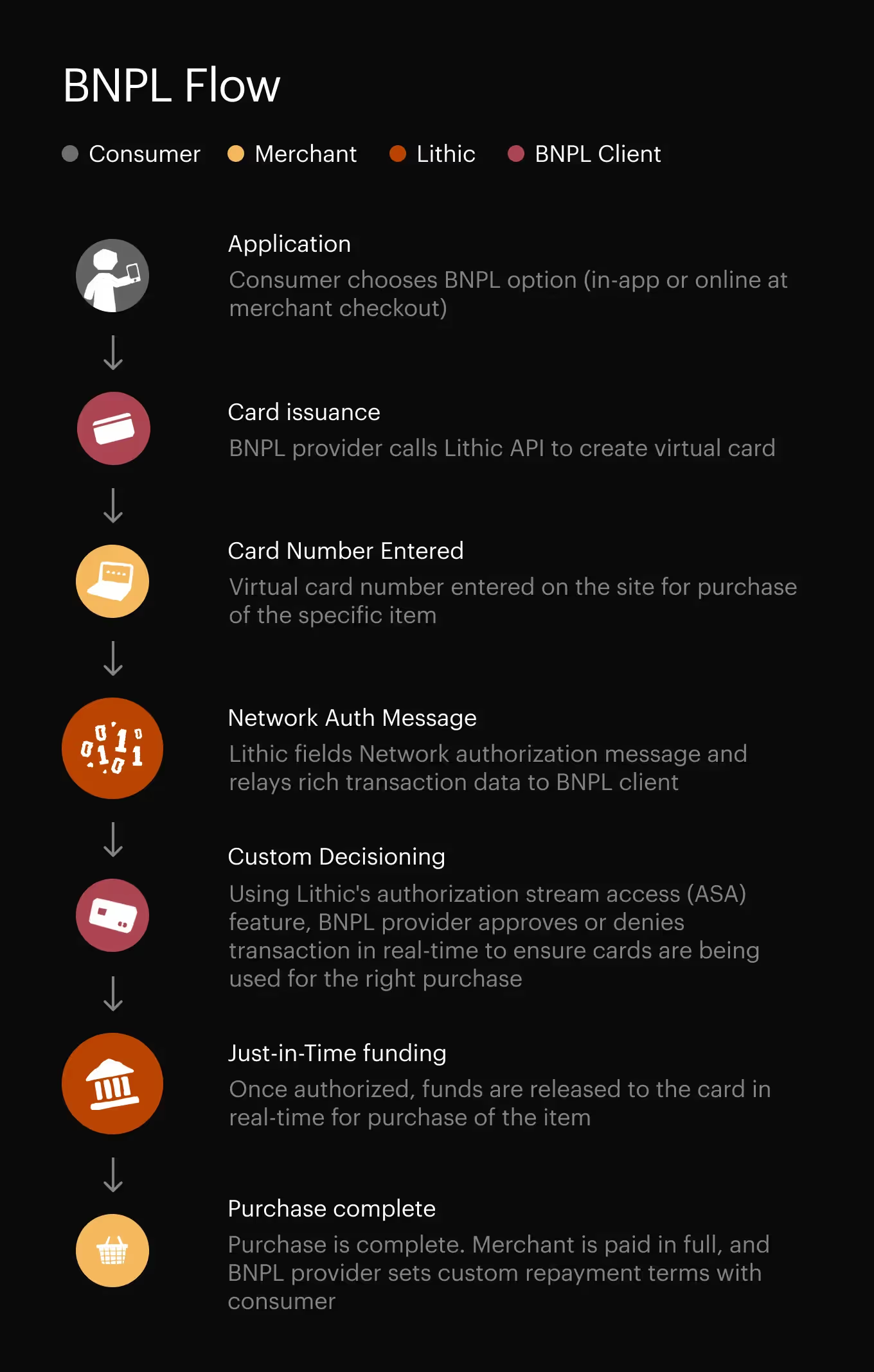

At Lithic, we recognize the exciting opportunity for early-stage fintech companies to accelerate the unbundling of the credit card industry. Lithic’s developer-first card issuing platform is built for flexibility. So no matter the BNPL use case, Lithic can help you bring your product to market in record time.

- Launching an in-app shopping experience? Instantly deliver single-use virtual cards to your customers and use Lithic’s Authorization Stream to approve/deny transactions in real-time based on criteria such as Merchant ID, MCC, and Amount.

- Issuing debit cards that give customers the option to split purchases into budget-friendly payments? Lithic can help you launch a fully-compliant, custom-branded card program with reloadable, physical cards, in a matter of weeks.

What’s more, Lithic’s card issuing platform is highly composable, meaning that you could plug and play our card issuing API into the best credit ledgering and loan servicing infrastructure providers in the market. Check out our Integration Partner Program to learn more.

We believe this is an exciting moment in time for new BNPL start-ups as well as many lending or credit-adjacent startups. If you’re building in the space, we’d love to hear from you. As the leading modern card issuing infrastructure provider, Lithic can be a fantastic partner for innovative founders and companies in the fintech industry.