Should founders and current financial-services execs go “all-in” on crypto and Web3? Or, should they play it safe and stay out of the fray?

In this blog, I make the case for a third way: the combination of crypto with best-in-class fintech.

This deep-dive also introduces the concept of “interoperability,” which refers to the need for infrastructure that allows consumers and businesses to move seamlessly between crypto and legacy banking and payments.

Crypto’s new innovation cycle

There’s a new cycle of innovation shaking up the world of crypto.

Among US consumers, awareness has been building and there’s significant adoption, particularly in the crucial demographic of ages 18 to 29. Among Americans of that age, 1 in 3 have traded or used cryptocurrency, according to a Pew Research Center survey released late in 2021.

And, below the surface, this cycle has been about company building as much as it has been about drawing in new enthusiasts with applications like NFTs and DAOs.

Coinbase’s IPO this year and rise to a $90B+ market cap demonstrated that the public markets had embraced crypto. And there’s a long list of companies riding Coinbase’s tail. In 2021 through September, crypto startups — companies building solutions atop blockchains or decentralized ledgers — drew $15 billion in funding globally, per CB Insights. That's already an increase of 384% over the full-year total in 2020.

The subcategory known as DeFi, or Decentralized Finance, was a major part of that story. DeFi accounted for $2.1B or 14% of the total dollars raised in the first 9 months of last year. Among the VCs and investors backing these DeFi startups in early rounds are some of the best and most respected firms: Andreessen Horowitz, Tiger Global Management, Lightspeed, and more.

Crypto vs. Web3 vs. DeFi

It’s always helpful when speaking about crypto to set down some definitions:

- Crypto: Here, we’ll use the term crypto to refer mainly to money powered by blockchain technology

- We’ll also refer to Web3: This, the buzzword of the moment, we take to mean the world of applications opened up by using the same blockchain tech to decentralize internet services.

- Decentralized Finance, or DeFi, is what’s encapsulated by the intersection of Web3 and crypto, as defined above. These are decentralized financial services that run on blockchains. Think lending, investing, payments, insurance, etc. without the legacy, traditional finance incumbents.

Moving beyond on ramps and off ramps

For consumers interested in crypto and Web3, the perennial problem has always been entering and exiting the market. While crypto may offer a new set of possibilities, consumers need government-backed “fiat” cash to operate in the real world. So, to move in and out of crypto, they must operate like foreign-exchange traders, constantly trading in and out of currency, at some cost.

This trading use case has historically been mediated by what are known as crypto “on ramps” — exchanges like Coinbase or payment apps like Cash — which allow for US dollar purchases of crypto, among other services. Off ramps operate in the other direction.

These on-ramps and off-ramps perform their core function well. But, arguably, the broader “job to be done,” unifying crypto with legacy financial and technical infrastructure, remains incomplete. While these on-ramp apps have paved the way to crypto adoption, and simplified the once-messy process of acquiring and trading cryptocurrency, they are still evolving in important ways. It will take a new innovation cycle, and perhaps new entrants, to open Web3 and DeFi services up in a way that will be accessible to most consumers.

For example, even a relatively simple use case like buying an NFT requires several steps beyond the “on ramp” in the present, including opening a crypto wallet, making sure it’s funded, and linking it to one of many NFT marketplaces.

Accessing a typical decentralized application or DeFi service involves even more complexity: a messy daisy-chain of fees, chains, wallets, passwords, alphanumeric hashes, and fear of botched transactions. In 2021, the internet might have been abuzz with chatter about “yield farming” — i.e. high returns from DeFi schemes — but only the technically-adept insider was positioned to seize the opportunities.

Broadly speaking, the world of crypto-powered financial innovation and Web3 remains relatively inaccessible to many, without a clear road marking the way forward for mass consumer or business adoption.

Where we’re headed: ‘highway interchanges’

It’s increasingly evident that what customers want isn’t a bifurcation of financial services. That is the past. In that world, which is increasingly in the rearview mirror, there’s a world with all-things-crypto on the one side and there’s legacy services — banking, lending, and stock trading — on the other.

What we are seeing today is consumers and startups pushing toward an exciting blurring of the two worlds. For a new generation of consumers and financial-market participants, there is no important distinction between their wealth in crypto assets and their savings in dollars. They want to be active in both the crypto market and the larger internet economy.

And, they want to do much more beyond moving their money in and out of crypto though on-ramps and off-ramps.

What comes next will be more like “highway interchanges,” API-based products that allow for a constant, high-volume flow of transactions between crypto and legacy financial services. Rather than provide a bridge for discrete transfers, i.e. “exchanges” in and out of crypto, this new generation of services will bridge the two worlds for many types of transactions, in real time and at scale.

This would mean new experiences in sending, spending, saving, and managing money in a way that straddles crypto and traditional fintech. In theory, a transaction could begin in any cryptocurrency or financial vehicle and end in any other. There would be a mind-boggling number of permutations and combinations.

Companies like Wyre, ZeroHash, Prime Trust, Paxos, Circle, and Ponto are already realizing this potential with their APIs.

- For example, ZeroHash’s developer-friendly API enables Tastyworks, an award–winning brokerage, to provide equity trading for customers who want to trade crypto and traditional stocks side-by-side

- Transak — through an embeddable widget or their API — helps businesses build products on top of at least 80 cryptocurrencies, across more than 100 jurisdictions, and 60 fiat currencies. Transak’s clients are able to offer solutions that are agnostic with regard to where the end customer sits on the spectrum in terms of familiarity with crypto.

- In one partnership, Wyre’s embeddable API allows the more than 20 million customers of a popular wallet, Metamask, to purchase and use ethereum tokens within any decentralized application (without having to interrupt what they’re doing or visit an exchange).

Taken together, these API-first products are evolving as a new infrastructure that fuse crypto and fiat transactions and make most of the complexity invisible to the user.

Seizing the growing market in ‘interoperability’

Hardcore DeFi and crypto advocates envision a world of “frictionless capitalism.” In this future, financial services are almost completely decentralized and crypto triumphs over government-backed currency.

It’s a long-term vision, and we may or may not see it come to pass. But what’s certain is that we are not there yet. Today an entire generation of customers want to harness the benefits of crypto alongside new fintech solutions based on software, cloud services, and APIs. This consumer demand is creating a massive market at the intersection of the two trends.

In other words, the massive opportunity is in crypto and fintech, together.

To better understand this market and its value, let’s turn to another concept, once borrowed from healthcare: interoperability. In healthcare, interoperability refers to a devilish challenge: medical data does not move easily between the various silos, including between different hospitals and clinics or between insurers and hospitals.

In fintech, interoperability means API-enabled, automated transfers of value between different financial products, protocols, and ecosystems, but also the smooth flow of other key pieces in parallel to the transaction. Which other pieces? It depends on context, but some financial operations may require participants’ identity to be carried along to comply with regulations, or there may be a need to register transaction status to different systems of record simultaneously, e.g. the credit-card networks, a blockchain, a company database, or all three.

We have already hinted at some of the applications made possible by this kind of interoperability above, when we mentioned a few API-first companies in crypto and fintech. But there’s a long list of use cases for these interchanges built on principles of interoperability, including:

- Borrowing and lending: In many contexts, the economics of lending are unwieldy. What’s missing is the automated matching of lenders to borrowers at a large enough scale to accommodate a wider range of loan products. If crypto is harnessed appropriately and connected with broad-based pools of capital, it should enable borrowing or funding of purchases and transactions of any amount and in many shapes and sizes.

- Wealth management: users who want to manage assets seamlessly across digital or crypto assets and traditional savings should be able to do so without switching apps or learning new protocols and behaviors

- Transfers: The clearing and settlement underlying any movement of money — even between crypto and fiat — should be completed instantaneously or near-instantaneously, with the help of APIs and algorithmic processes

There are many more use cases, of course. The combination of fiat and crypto allow for quite a few permutations. The use cases marry the ubiquity and depth of traditional financial markets with the programmability and technical soundness of crypto, and that means there are more, not fewer possibilities.

Below, we’ll speak to one immediate opportunity in interoperable financial services: payment cards.

Crypto credit, debit, and rewards

A fundamental problem in crypto are the walls between the various “holding pens” for crypto wealth and the traditional consumer economy. To put it bluntly: the various wallets, exchanges, and other core crypto services are locking in billions of dollars in spending power.

In an extreme case, Bitcoin’s pseudonymous creator, Satoshi Nakamoto, holds the equivalent of more than $70B in a Bitcoin wallet, wholly outside of the traditional banking system.

Putting aside this extreme case, what if crypto wealth could more easily be spent in the real economy?

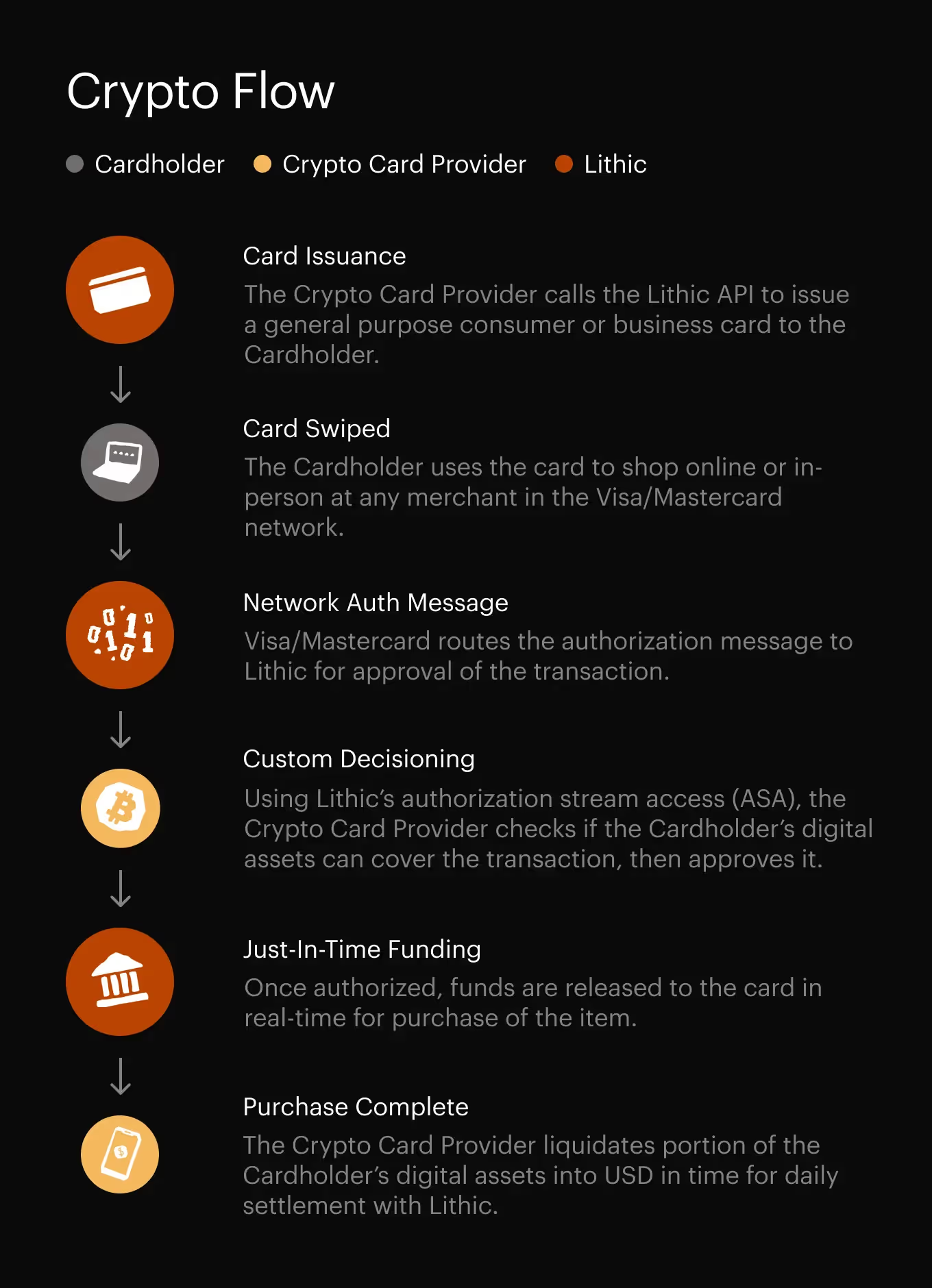

An immediate opportunity is in payment cards. Here, the floodgates of innovation are already open. Today, debit and credit card programs, tied to crypto accounts, are arguably the best and most convenient technology for consumers to use if they want to spend crypto in the traditional economy.

For consumers, credit and debit cards bring clear benefits:

- Instant and seamless spending: Crypto-linked cards mean customers would be able to spend crypto wealth as easily as they would be able to spend U.S. dollars

- Peace of mind by staying fully invested in crypto: A less obvious benefit is that customers can keep holding as much crypto as they want, rather than having to exchange lump sums ahead of time to fund purchases. They can keep as much of their savings in crypto as they like, and have the flexibility to spend on a transaction-by-transaction basis.

- Crypto-rewards program possibilities would be endless: It’s not difficult to imagine new reward programs engineered around innovative perks like “earn Bitcoin-back” or “members-only NFT access,” tokenized points, and more.

Roughly speaking, there are four profiles of crypto organizations that are attractive candidates for launching their own debit or credit card programs. The below is far from an exhaustive list, and will no doubt grow in the next year as new business models and product categories emerge.

- Exchanges: Exchanges are perhaps the most obvious candidates to have their own cards, which would draw on customer accounts but also tap into exchanges’ ability to exchange crypto in real time and move value between currencies. A customer of an exchange-branded credit card might choose what cryptocurrency to use when making purchases.

- Wallets: Wallets are the key utilities in the world of crypto, and while exchanges get more attention, many wallets are seeking to expand their relationships with customers with new products and services

- Crypto-powered “bank-like or bank-lite” services, including savings and lending apps: A fast-growing ecosystem of companies and products lean on crypto to anchor personal financial management, corporate treasury, and other financial services offerings. For example, one category is gamifying personal finance with a crypto lens, encouraging behavior like savings, smart spending, and crypto diversification.

- Other products: custody services, NFT projects and NFT marketplaces, etc. A significant proportion of crypto wealth is held in a long tail of other products, and it should be possible to build credit and debit programs on top of many of them.

For companies in crypto considering card programs, there are a few advantages to consider. One advantage is the possibility of a clear differentiator vs their competition, and another is a new source of customer engagement. But most concretely, a card has the potential to be a significant revenue source in its own right, since a company launching a card program would collect revenue from fees on the customers’ spending volume.

So, what’s next?

Early-stage companies at the intersection of crypto and fintech are building a new generation of financial services. To do so, they are in need of an infrastructure that can manage the accelerated pace of change and adapt with them.

The future is highly uncertain when it comes to crypto, DeFi, and Web3, and perhaps it is too early to bet aggressively in the direction of fully decentralized finance.

But we can take a page from Jeff Bezos’s strategic playbook when planning for the future and think about what won’t change. With that in mind, it seems safe to say that no matter what the future holds, businesses and consumers will need reliable and smooth paths for moving money between the traditional and crypto economies.

And that’s why businesses have a massive opportunity in promoting interoperability and seamless movement between the two worlds. Credit and debit card programs are already a tested way to help that happen, but they are only one option at the intersection of crypto and fintech.