%20(2).png)

Lithic has supported consumer revolving credit programs for years through our direct-to-network processing and integrated third-party ledger provider partnerships. Today, we’re excited to announce an expansion of that support with the launch of a native consumer revolving credit ledger, which brings the same infrastructure depth and thoughtful design that has long powered our commercial revolving programs directly to consumer use cases as well.

What It Takes To Build Revolving Credit Right

Revolving credit is one of the most complex products in fintech to build and operate, as well one of the most consequential to get right. The cardholder experience looks deceptively simple: spend, receive a statement, pay some or all of it back, repeat. The infrastructure underneath tells a different story.

Behind each step of the revolving credit cardholder lifecycle are infrastructure decisions that compound quickly: a ledger that tracks balances across multiple categories simultaneously, an interest calculation engine that accrues daily and recalculates retroactively when needed, payment logic that allocates payment funds in a specific regulatory order, and a statement layer that surfaces precise disclosures on a fixed timeline.

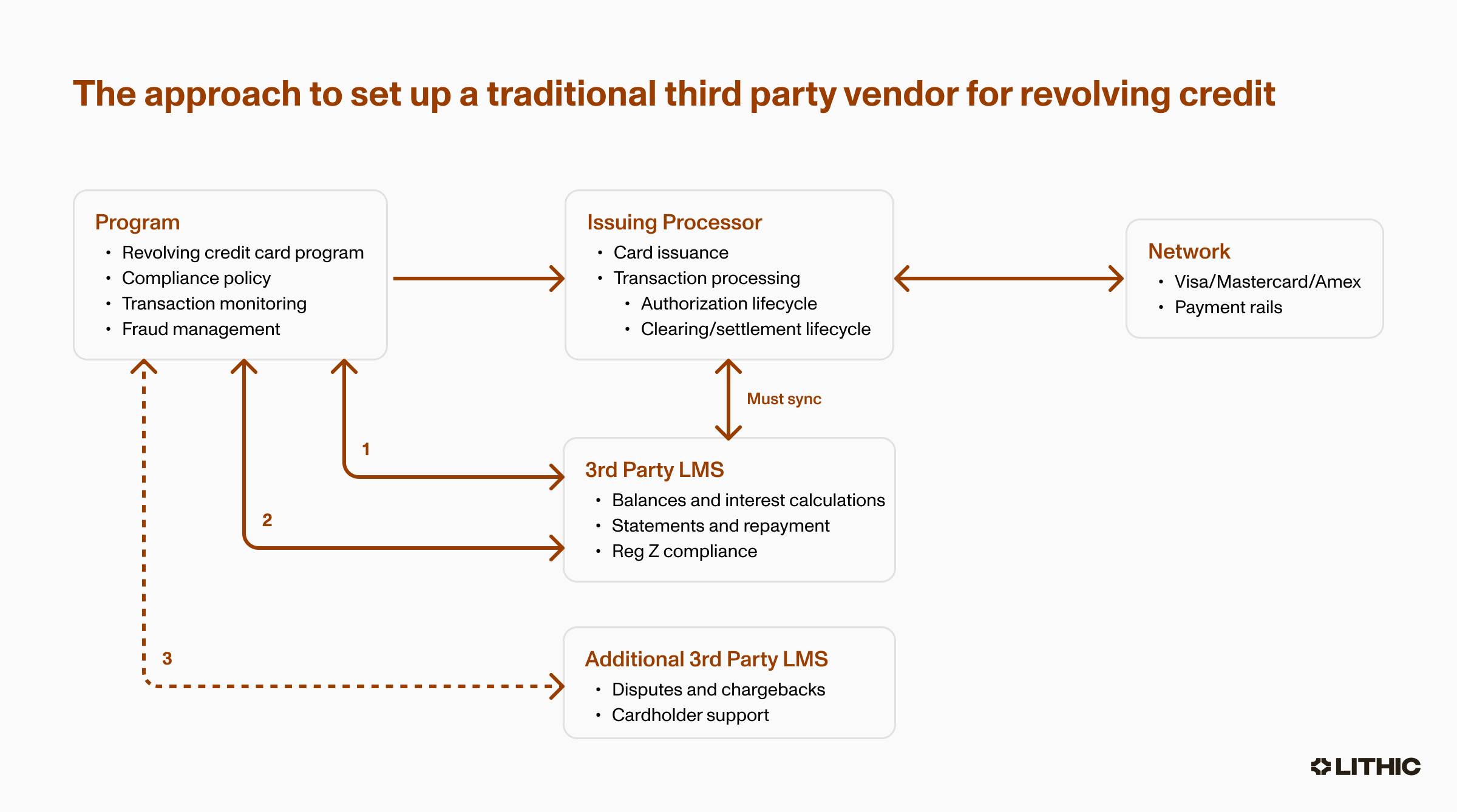

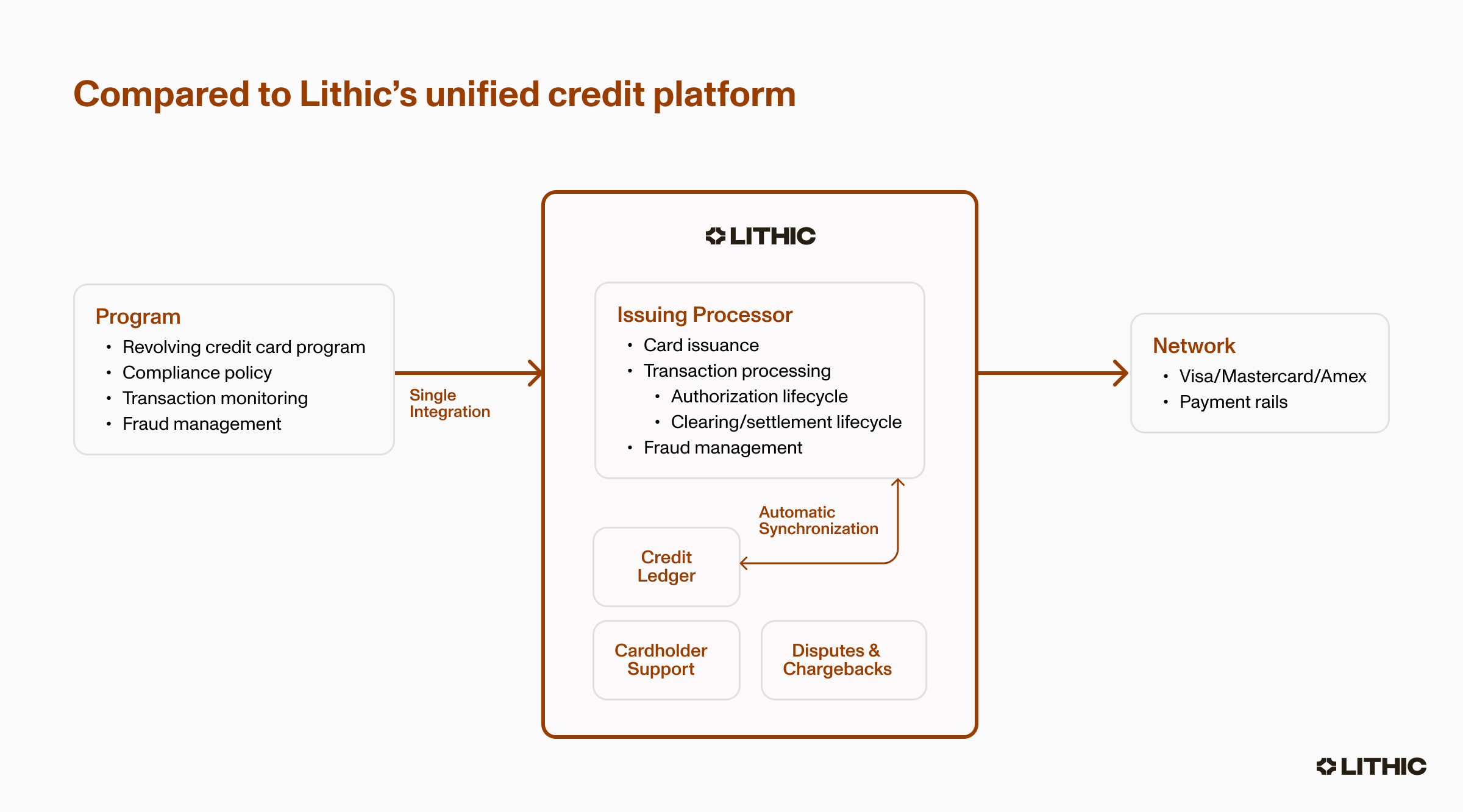

Consumer programs add another dimension: the legal framework governing consumer credit was crafted from a consumer protection mindset, not logical technical specs. Regulation Z imposes detailed requirements on interest calculations, fee structures, and disclosures that are genuinely tricky to implement correctly. Programs that choose an issuer processor that fails to deliver any one of these aspects risk generating regulatory inquisition and undermining cardholder trust. In order to meet these complex requirements, legacy providers force a tradeoff between compliance coverage and program flexibility, which compels programs to then potentially seek third-party credit integrations on top of their processing stack. Lithic delivers it all in a single platform.

The Lithic team has done the complex work of translating the regulatory framework into digestible software that clients can leverage to stand up custom credit programs. Moreover, Lithic is able to support both commercial and consumer revolving credit programs with compliance capabilities built directly into the infrastructure. We abstract the complexity of credit mechanics and compliance, which makes Lithic the platform of choice for fintechs building the most sophisticated revolving credit products in the market.

Flexible Program Configurability

Generic credit infrastructure forces programs to accept a rigid rate and fee structure that doesn't quite fit their product or try to build custom logic on top of a platform that wasn't designed to be flexible. Neither option is tenable for modern card programs seeking to launch unique programs.

A secured consumer card, a general-purpose rewards card, a cobrand retail card, and an embedded credit product for a vertical SaaS platform each require different rate structures, fee logic, and billing mechanics. The infrastructure underneath needs to be flexible enough to support all of them without requiring custom engineering for each variant.

We designed our platform’s credit configuration layer around this principle. In practice, this means that programs can:

- Configure distinct APRs for each category of transaction, including promotional and penalty rate optionality for maximum flexibility

- Set tiered APRs by customer segment or individually on each customer account. APRs can also be prime-linked for variable rate programs that adjust automatically when the prime rate changes

- Customize billing cycles to be fixed to a calendar date or rolling from account opening, with configurable grace periods up to the length of the billing cycle, with per-account tracking of eligibility

- Automate fee logic (e.g., late payment, returned payment, foreign transaction, annual, and cycle fees) based on program set-up, with maximum occurrence caps per billing cycle, so the platform enforces your fee rules without you monitoring for trigger events

- Manage credit limits at both the business, cardholder, and card level, with API-driven adjustments and temporary increase support

- Adjust highly configurable Minimum Payment logic. Control specific categories included in the minimum payment, set a percentage, or a fixed minimum payment amount

Two capabilities in particular reflect the operational depth and precise, programmatic control that programs need to support credit situations. Programs often need to schedule APR adjustments tied to specific triggers or timeframes, such as a promotional rate expiring or a penalty rate engaging after missed payments. Scheduled APR challenges allow clients to program these changes natively so these transitions execute on the exact intended workflow timeline.

On top of precise interest calculations, our ledger also supports pausing interest accrual and fee assessment at the account level for programs that seek to offer hardship accommodations including bankruptcy proceedings, automatic charge-off processes, promotional windows, or regulatory grace periods for creditor interest relief.

Lithic’s revolving credit infrastructure enables clients to make thoughtful program design decisions reflective of their goals and cardholder base.

Regulation Z: From Law to Ledger

Consumer revolving credit carries compliance obligations that go well beyond accurate accounting. Regulation Z, the implementing regulation of the Truth in Lending Act, specifies what must be disclosed on every statement, how interest must be calculated, and how payments must be applied. These requirements were written for consumer protection, not for ease of implementation and platform software development. The investment to translate that legal logic into correct, auditable software behavior is significant: months of engineering time, ongoing maintenance as interpretations evolve, regulatory exposure, and potential cardholder complaints should anything fail.

Our revolving credit platform accounts for each of these legal considerations. Lithic solved these challenges so that your program doesn’t have to.

Payoff disclosures: Every consumer credit statement must show how long it would take to pay off the current balance making only minimum payments, the total cost of doing so, and the monthly payment that would retire the balance in 36 months. These require running a full amortization model against each account's balance, rate, and minimum payment formula—correctly, every cycle. Even one missed disclosure is a compliance failure. The Lithic platform calculates all of it automatically and surfaces the results in the statements API, ready to render.

Retroactive interest calculations: When a posting adjustment happens (like a chargeback dispute), interest may need to be recalculated from prior periods. Errors in the retro calculations will generate disputes and potential remediation. Lithic handles retroactive interest automatically, including the calculations required for MLA and SCRA compliance.

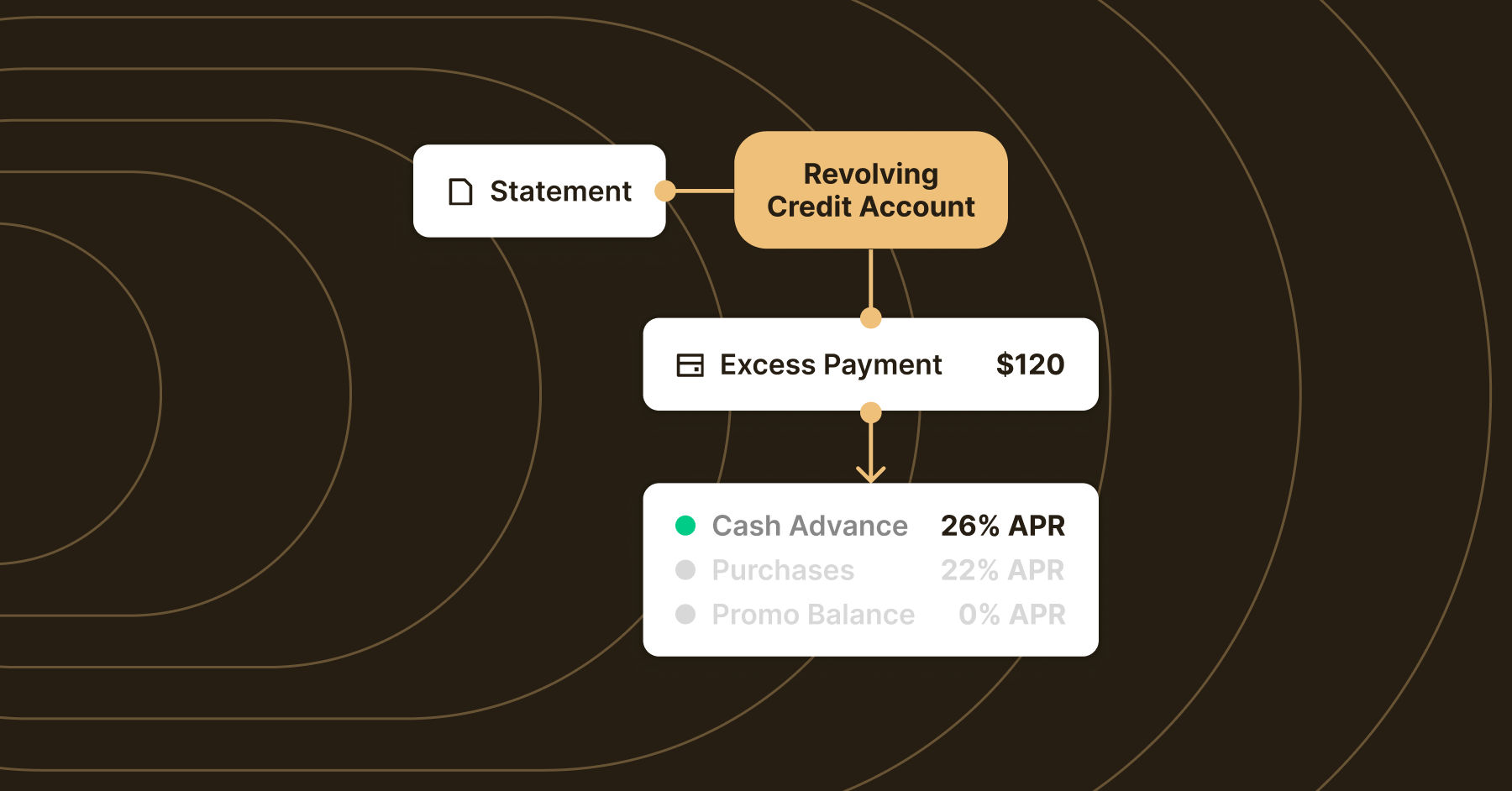

Payment allocation disclosures. Regulation Z specifies how payments above the minimum must be applied: to the highest-APR balance first. Lithic’s payment engine follows this allocation order automatically. The statement reflects exactly how each payment was applied, so there's an auditable record without any program-side logging.

APR and interest breakdowns by category. Statements must separately disclose APRs and interest charges for each balance type. Our interest engine tracks all of this at the category level throughout the billing cycle, and surfaces the full breakdown in statement data, including the calculation method, prime rate where applicable, and actual versus minimum interest charged.

Days past due and account standing. The Lithic platform tracks days past due, consecutive minimum payments made and missed, and consecutive full payments at the account level, surfacing this in every statement. This data drives delinquency and charged-off workflows, penalty rate triggers, and the cardholder communications that Reg Z and the CARD Act require.

One Extensible Platform

The same infrastructure that powers Lithic's commercial revolving credit programs now covers consumer as well: comprehensive card issuing and processing, Authorization Intelligence for fraud decisioning and controls, immutable ledgering with to-the-penny reconciliation. Multi-tenancy companies that serve both individual and business cardholders, or that plan to expand to additional programs, don't have to stitch together separate infrastructure to do it.

This is what makes Lithic the right platform for companies building complex, differentiated revolving credit products—a complete infrastructure layer that handles the hard parts so programs can focus on building their best cardholder experience.

Explore Lithic's revolving credit documentation or talk to our team to learn how we can support your credit program.